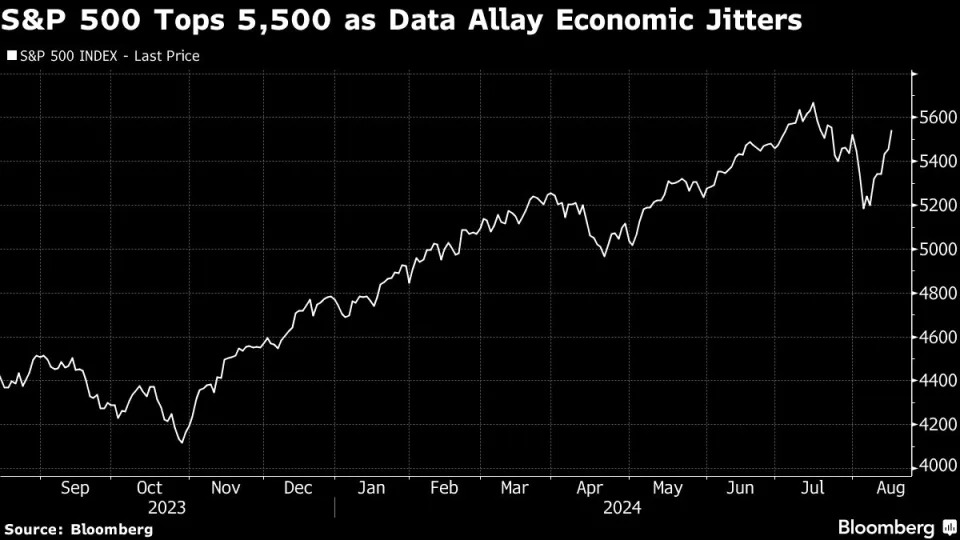

Stock market valuations are looking stretched as 2024 winds down, and it's got some market watchers on edge — but investors shouldn't fear, UBS says, as prices are justified and set to keep climbing.

At 22.2x, the S&P 500's forward price-to-earnings ratio is far above its average of 16.8x over the last 30 years, and close to its 25.0x record high reached during the dot-com bubble in 1999.

Strategists have warned that such stretched valuations mean stocks are due for a correction and are at risk of a painful decline in the event of even mild disruptions.

Analysts at UBS, though, argued such elevated stock valuations are justified—and will climb higher next year—in a note this week titled "22x and Beyond: The Case for Higher Valuations, or How to Worry Less and Love the Market."

The strategists, led by Jonathan Golub, pointed first to the tech sector's growing dominance in the S&P 500.

Around 30 years ago, before the rise of the internet and long before the smartphone, tech-related companies made up just 10% of the S&P 500's market cap. Now, they account for 40%.

At the same time, tech firms have grown their top lines quicker and with higher margins, with sales growth surging almost 11% and margins up 24%, compared to 6% sales growth and 13% margin growth for non-tech stocks.

"The result—not surprisingly—is an upward short in valuations for the market broadly," they said in a Monday note.

Meanwhile, both tech and non-tech stocks have seen improved cash flows as they become less capital-intensive, the analysts said. The greater cash flows return more to shareholders, helping stocks naturally trade at higher price-to-earnings ratios, they added.

They also pointed to lower discount rates, with the current 10-year Treasury yield 40 basis points above its long-term average, while credit spreads are 220 basis points lower. Together, that makes for a 20% decrease in the cost of capital versus the historical average, which helps to explain part of the reason for such high valuations, the analysts said.

Lastly, they noted that valuations rise in non-recessionary periods, meaning valuations will likely continue their upward trend next year.

"With current recession risks contained, multiples are most likely to drift higher in 2025," they said.

The firm's analysis comes as S&P 500's bull rally has pushed the benchmark index up 28% in 2024, as tech stocks boom and the economy remains on solid footing.

The stock rally saw a fresh catalyst last month with Donald Trump 's reelection, which has fueled hopes of sustained earnings growth as a result of less regulation and lower taxes.

Read the original article on Business Insider