(Bloomberg) -- Stocks retreated after a rally that put the market on pace for its best year since 2019, with traders awaiting key inflation data that will help shape the outlook for Federal Reserve rates.

The S&P 500 dropped from nearly overbought technical levels, following a series of all-time highs. Nvidia Corp. slid as China opened a probe over suspicions the giant US chipmaker broke anti-monopoly laws around a 2020 deal. Meantime, Chinese stocks that are listed in the US staged a sharp rally as top leaders in Beijing used their most direct language yet on providing monetary easing and boosting domestic consumption.

Data including Wednesday’s consumer price index will offer Fed officials a final look at the pricing environment ahead of their meeting the following week. Any indication that progress has stalled on the inflation front could well undercut the chances of a third straight reduction in rates.

“This Wednesday’s inflation data may hold the key to the Fed’s next move,” said Jay Woods at Freedom Capital Markets. “So far results have been in line with economists’ expectations and haven’t scared the market. However, an upward surprise should raise eyebrows at the Fed and could put another rate cut on pause.”

To Chris Larkin at E*Trade from Morgan Stanley, only a dramatic CPI increase would prevent the Fed from cutting rates in December.

The S&P 500 fell 0.6%. The Nasdaq 100 slid 0.8%. The Dow Jones Industrial Average lost 0.5%.

Treasury 10-year yields rose four basis points to 4.20%. The Bloomberg Dollar Spot Index rose 0.1%.

Oil climbed as China signaled bolder stimulus for next year, with traders also keeping an eye on developments in the Middle East.

“On the CPI and other inflation metrics, progress has stalled in recent months,” said Greg McBride at Bankrate. “This upcoming release will be closely scrutinized to see if there is evidence of renewed inflation pressures or signs of further improvement. “The rate of inflation has moderated significantly from a peak of 9 percent in 2022, but remains well above the target of 2%.”

The median projection in a Bloomberg survey of economists calls for a fourth consecutive 0.3% month-over-month increase in the November core CPI, which excludes food and energy for a better snapshot of underlying inflation. On an annual basis, the core measure probably rose 3.3% for a third month.

“That sort of pace is riding the edge of acceptable inflation levels, highlighting the importance of this week’s release, said Jason Pride and Michael Reynolds at Glenmede. “The Fed is likely leaning toward a 25 basis-point rate cut next week, but only if it is reasonably confident that inflation issues are not re-emerging.”

To Neil Dutta at Renaissance Macro Research, those seeing an inflationary boom keeping the Fed from lowering policy rates can’t use the labor market to press their case.

“A continued cooling in the labor market keeps monetary easing in place,” he noted.

“While the start of Fed easing, the clearing of election uncertainty and ‘animal spirits’ have sustained the bull market, investors have more recently been inundated with arguments linked to market technicals,” said Lisa Shalett at Morgan Stanley Wealth Management. “It is generally good advice to never ‘fight the Fed’ or ‘the tape’.”

She bets positive technicals and seasonality may power US equities another 5%-10%.

“While bears argue that the year-end rally reflects stalling trading volume or ‘window dressing’ by market participants, bulls highlight favorable seasonal tailwinds, calm risk factors, and a supportive fundamental backdrop,” said Mark Hackett at Nationwide. “This optimism, coupled with resilient November jobs data, has helped major equity indexes reach new record highs despite lingering concerns about Fed policy, labor market risks, and geopolitical unrest.”

The S&P 500 will extend its record-setting rally to 7,100 by the end of next year amid a strong economy, according to Oppenheimer Asset Management, whose outlook is now the most bullish among peers.

Fundamentals “suggest the current resilience of the economy and the stock market appear poised to continue into next year,” the firm’s Chief Investment Strategist John Stoltzfus wrote in a note.

Citigroup Inc. strategists expect mid-single-digit gains for the S&P 500 in 2025 amid increasing volatility, fueled by a soft landing of the US economy, artificial intelligence and Donald Trump’s policy promises.

Their base-case target is 6,500 points for the S&P 500. The upper scenario is set at 6,900 and lower at 5,100; both the bull- and bear-case scenarios “frame an expectation for increased volatility,” the strategists wrote.

Post-election euphoria and seasonal tailwinds set US equities up for a banner autumn, and so far the positive fall performance is a sign gains can continue even when the calendar year turns, if history is any guide.

Since 1930, after better-than-usual returns in November and December, the S&P 500 has posted a median 3% gain in the subsequent first quarter and has risen more than two thirds of the time, according to Bloomberg Intelligence’s strategists Gina Martin Adams and Michael Casper. That means the US stock benchmark’s nearly 6% advance last month is helping set the index up for more upside in January, so long as stocks continue their climb over the next few weeks.

Hedge funds net bought US equities for the first time in four weeks with macro products, such as indexes and exchange-traded funds, making up nearly 90% of the net buying, according to Goldman Sachs Group Inc. prime brokerage desk’s report for the week through Dec. 6.

Single stocks were modestly net bought, with long buys slightly outpacing short sales. Hedge funds net bought information technology stocks at the fastest pace in seven weeks, though the sector is still net sold over the past month. Industrials was the most net sold sector with last week’s notional short selling being the largest in more than two years.

Buyside US equity futures positioning has moved slightly lower after hitting a new all-time high, while some investors expect see a “significant pullback” on the horizon, according to strategists at RBC Capital Markets led by Lori Calvasina.

Investor exposure to stocks remains above average, but is not at extreme levels, according to Deutsche Bank AG strategists led by Parag Thatte.

Exposure of discretionary investors has pulled back after the post-election surge but remains elevated, they noted. Positioning in mega-cap growth and tech stocks is elevated, while the gap between cyclicals and defensives has closed. Exposure to small caps is near the top of its historical band.

Corporate Highlights:

Key events this week:

Some of the main moves in markets:

Stocks

Currencies

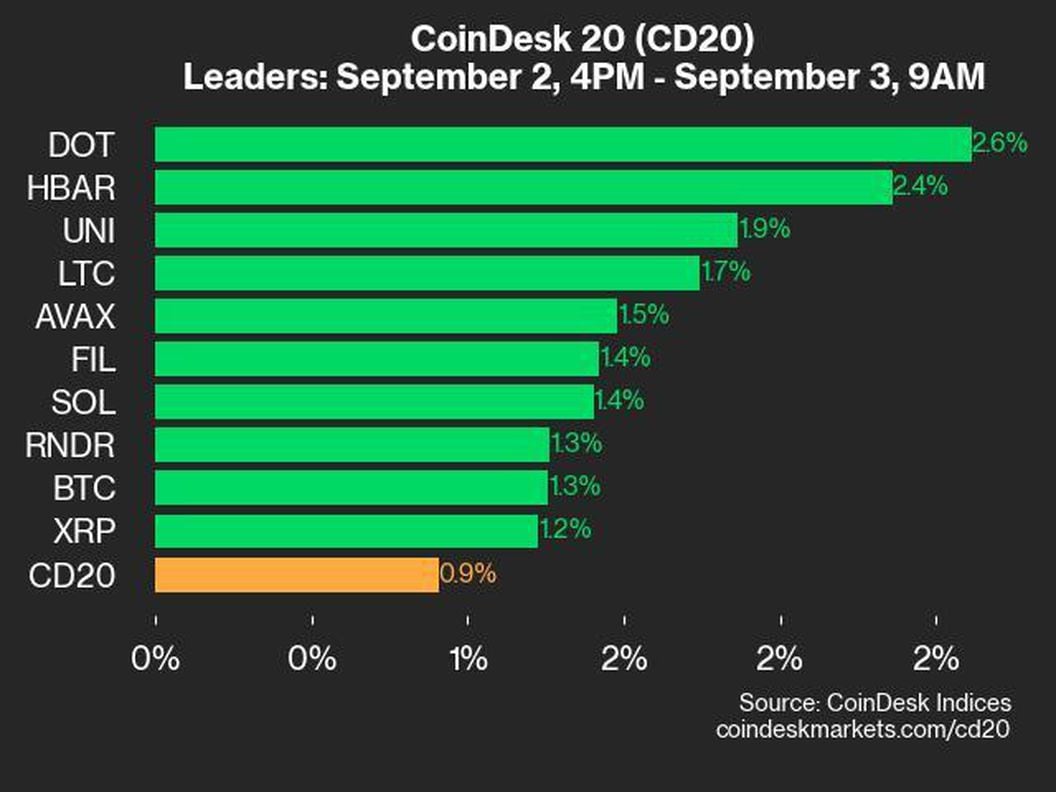

Cryptocurrencies

Bonds

Commodities

This story was produced with the assistance of Bloomberg Automation.