Michael Saylor, the founder of MicroStrategy, has become one of Bitcoin’s most vocal advocates, boldly proclaiming, “There is no second best.”

Since 2020, Saylor has leveraged his publicly traded company to amass over $14 billion in paper profits by buying more than $30 billion worth of Bitcoin, positioning MicroStrategy as the largest corporate holder of the cryptocurrency. It’s a strategy that has drawn admiration from Bitcoin maximalists and skepticism from traditional investors alike.

But as MicroStrategy continues to raise billions in capital — targeting $42 billion in new funding over the next three years — to quadruple down on its Bitcoin bet, concerns are mounting. Could this be the makings of another massive bubble? And if Bitcoin’s price falters, how will MicroStrategy’s bold play end?

The Ghost of Trades Past

MicroStrategy’s Bitcoin strategy has parallels to one of crypto’s most infamous trades: the “GBTC Premium Trade.” At its height, this arbitrage opportunity allowed investors to leverage Bitcoin exposure through Grayscale’s Bitcoin Trust (GBTC), which traded at a premium to its underlying Bitcoin holdings. Many investors took out loans to exchange that money for GBTC shares and pocketed profits from the premium after a lockup period .

The trade unraveled spectacularly in 2021 when the GBTC premium flipped to a discount. Firms like Three Arrows Capital and BlockFi, which had leveraged themselves heavily or exposed themselves to people who had levered up, imploded. The ensuing wave of bankruptcies, including Genesis, highlighted the dangers of building financial strategies on fragile market inefficiencies.

Today, critics warn that MicroStrategy is walking a similar tightrope. But instead of leveraging GBTC’s premium, MicroStrategy is opening a new path to levered bets on Bitcoin using its own stock and bonds — essentially turning the company into a Bitcoin proxy with added leverage.

The Magic of Convertible Debt

MicroStrategy’s strategy hinges on raising capital through convertible bonds and equity offerings. Here’s how it works:

-

Borrow at Low Rates (0%) - MicroStrategy offers bondholders minimal or zero interest rates.

-

Offer Stock Upside - Instead of interest, bondholders are allowed to convert their bonds into MicroStrategy shares if the stock price rises. This potential upside has attracted major institutional players, including Allianz, Germany’s largest insurer.

-

Buy More Bitcoin - The capital raised is then funneled into additional Bitcoin purchases, fueling further stock price gains.

This feedback loop has propelled MicroStrategy’s stock to staggering heights, climbing nearly 500% in 2024 alone. The strategy has been so effective that bond investors have lent the company billions at 0%, lured by the potential to convert bonds into shares worth more.

It’s a compelling pitch: why settle for a low-interest return on bonds when MicroStrategy offers the chance to double — or even quintuple — your investment? As Saylor put it in a recent investor call, bondholders are escaping a world of “negative real returns” for a taste of Bitcoin’s upside.

For now, MicroStrategy’s strategy has worked brilliantly, creating a virtuous cycle as Bitcoin’s price rises. But what happens if Bitcoin’s trajectory reverses?

MicroStrategy owns nearly 387,000 bitcoins, valued at approximately $37 billion, but its stock market valuation exceeds $100 billion. This outsized valuation relies heavily on the assumption that Bitcoin’s price will continue climbing. If Bitcoin falls, the company’s stock — essentially a levered bet on Bitcoin — could crater.

Consider also that 2x levered ETFs, like MSTU and MSTX, dedicated solely to MicroStrategy have also fueled the speculation on top of MicroStrategy's Bitcoin speculation.

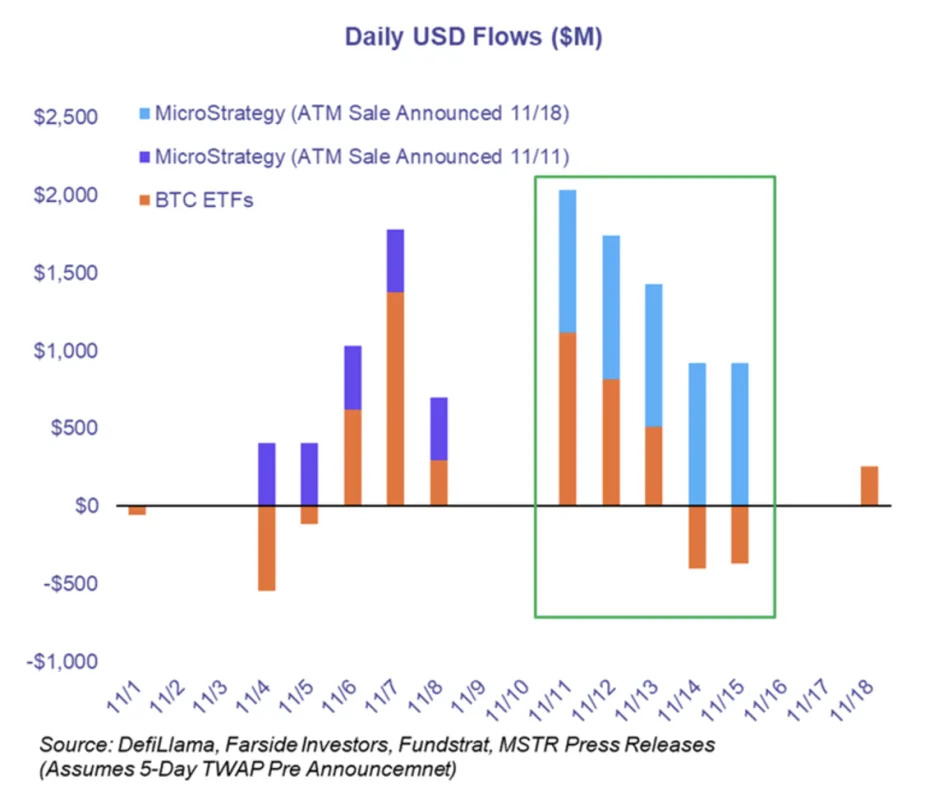

All of that has amounted to incredible added Bitcoin buying. In fact, buys from MicroStrategy actually dwarfed inflows from all of the Bitcoin ETFs combined earlier this month, according to Fundstrat research. If the market begins to doubt MicroStrategy might be able to reach its $42 billion target, Bitcoin's price could fall and further endanger MicroStrategy's ability to raise capital. And once that flip switches, things can get ugly fast. The same was true for FTX's attempts to raise money when they needed it most , and for Terra in its $40 billion collapse .

While Saylor has repeatedly stated that the company would never sell its Bitcoin, this position could become untenable if debt obligations mount and Bitcoin’s price declines.

Lessons from History

The cautionary tale of the GBTC Premium Trade looms large. That bubble burst when market conditions shifted, exposing the fragility of leverage-based strategies. MicroStrategy’s approach may avoid some pitfalls of the GBTC trade — it doesn’t rely on an inefficient fund structure — but it shares the core risk of leverage magnifying losses if Bitcoin prices drop.

Saylor’s unshakable faith in Bitcoin may inspire confidence, but history suggests that markets don’t rise indefinitely. Much like the Terra collapse in 2023, when overconfidence in a self-sustaining system led to a $40 billion wipeout, MicroStrategy’s stock could face a similar reckoning if Bitcoin prices falter.

But for Bitcoiners who are convinced the U.S. government is next in line to add Bitcoin to its balance sheet via a Strategic Reserve, MicroStrategy's bet has the potential to go down as the greatest of all time — famously genius, or infamously not.