ACT Research forecasts market upswing in 2025

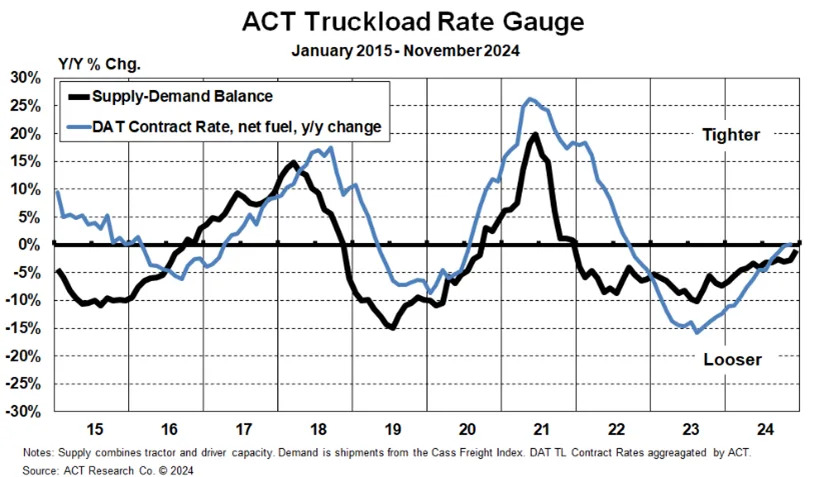

If 2024 was considered a freight market rebalancing for truckload, then 2025 is projected to be the end of the freight recession in the for-hire space, according to ACT Research . Its 58-page freight forecast paired aggregate spot data provided by DAT with a proprietary Supply-Demand balance curve. In the release, Tim Denoyer, vice president and senior analyst at ACT Research, said, “Currently, with a significant capacity contraction by for-hire fleets and private fleet insourcing slowing, capacity has finally rebalanced enough for rates to start moving higher.”

Using data provided by DAT, Denoyer adds that spot rates net of fuel are 7% higher than one year ago in Q4, while data provided by DAT, Cass Information Systems and fleet financial data shows modest increases in contract rates.

SONAR spot rates net of fuel were more optimistic, up 14.7% y/y from $1.63 to $1.87 as of Nov. 26. The FreightWaves National Truckload Index (Linehaul Only) estimates its fuel surcharge “based on the average retail price of diesel fuel and fuel efficiency of 6.5 miles per gallon. The formula is NTID – (DTS.USA/6.5).” Comparing Q4 2023 to Q4 2024 quarter to date shows an average linehaul rate of $1.60 versus $1.74, an increase of 8.75% as of Nov. 26.

Denoyer adds a caveat, as the extent of the boom in 2025 may be less than predicted due to private fleet expansion: “The market is very close to balance, and in 2025 the combination of normalizing equipment supply and a pre-tariff safety stock build are poised to drive higher for-hire freight demand and rates. The big private fleet expansion of the past two years will likely still leave anyone looking for a boom disappointed, but the for-hire rate recession is finally over,”

Schneider National grows dedicated revenue to $2 billion with Cowen purchase

Schneider National is acquiring Cowan Systems for approximately $390 million in cash, including real estate assets with around $31 million. Baltimore-based Cowan Systems includes dedicated assets in addition to a brokerage, drayage and warehousing component. The 100-year-old company has approximately 1,800 trucks and 7,500 trailers spread across over 40 locations in the Eastern and Mid-Atlantic regions. The purchase, announced Monday, will add to Schneider’s existing 8,400 dedicated tractors, raising its truckload fleet to over 70% dedicated. Prior to its acquisition blitz, Schneider had 4,498 dedicated trucks at the end of 2021.

FreightWaves’ Todd Maiden writes , “Schneider’s annual dedicated revenue is now close to $2 billion with its consolidated revenue likely moving above $6 billion.” Part of the purchase is coming from a new credit line. Maiden adds, “Schneider will use cash on hand and a new $400 million credit facility to fund the acquisition, which is expected to close before year-end.”

Schneider’s acquisition follows previous expansions in the dedicated space. Additional recent acquisitions include its purchase of Midwest Logistics Systems , a 900-truck dedicated fleet, for $263 million in January 2022 and 500-truck fleet M&M Transport Services in August 2023 for an undisclosed sum. Following these acquisitions, Schneider is now one of the largest dedicated transportation providers in the United States.

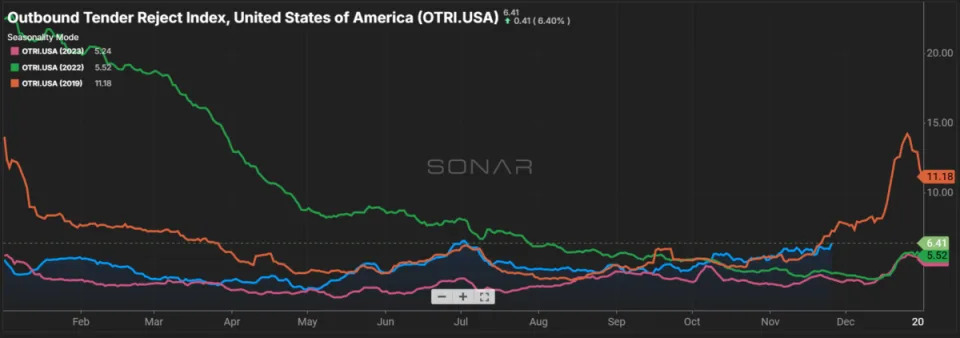

SONAR spotlight: The return of holiday seasonality may create a December to remember

Summary: Nationwide outbound tender rejection rates continue to climb, as Thanksgiving repositioned trucking capacity ahead of the holiday on Thursday. The current sustained uptick in rejection rates more closely mimics 2019 than the previous two years, when an uptick was not observed until mid-December. The past week saw the Outbound Tender Reject Index increase 84 basis points from 5.57% on Nov. 18 to 6.41%. Compared to this time last year, OTRI is 257 bps higher than 3.84% on Nov. 25, 2023.

Breaking down the nationwide index by segment saw gains across the dry van, flatbed and reefer segments. Dry van saw the smallest gain, up 66 bps w/w from 5.02% to 5.68%. Reefer rose 318 bps w/w from 13.45% to 16.63% while flatbed was up 375 bps w/w from 10.53% to 14.28%. Expect further increases in tender rejection rates as truckload capacity tightens leading into and coming out of the Thanksgiving holiday. Facilities closures at shippers, terminals and brokerages may also impact the tender rejection rate, as appointments are pushed out or load times adjusted.

Dry van spot market rates also showed a holiday uptick, and all-in rates continue to outperform compared to this time last year. The FreightWaves National Truckload Index 7-Day Average rose 6 cents per mile w/w from $2.37 on Nov. 18 to $2.43. The NTID, the daily movements in the NTI which feed the seven-day average, spiked ahead of the holiday, with the NTID’s reading on Sunday of $2.84 at its highest level since Dec. 25, 2022. The NTID is a more volatile dataset compared to the NTI 7-Day average, but that high one-day reading suggests higher spot rates over the next week.

The Routing Guide: Links from around the web

FMCSA to move ahead with revamped CSA scores (Overdrive)

November 2024 For-Hire Trucking Index (ACT Research)

Kenan Advantage Group acquires 2 more dry bulk carriers (Trucking Dive)

UPS hit with SEC fine over its internal valuation of UPS Freight before TFI sale (FreightWaves)

OTR division of 38-year-old Texas carrier ‘absorbed’ by MVT

(FreightWaves)

Florida extends hurricane emergency, South Carolina DOT to replace 10 bridges

(Land Line)

Like the content? Subscribe to the newsletter here.

The post ACT Research forecasts market upswing in 2025 appeared first on FreightWaves .