PVH has been treading water for the past six months, recording a small loss of 3.1% while holding steady at $94.84. The stock also fell short of the S&P 500’s 12.6% gain during that period.

Is there a buying opportunity in PVH, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free .

We're sitting this one out for now. Here are three reasons why we avoid PVH and a stock we'd rather own.

Why Do We Think PVH Will Underperform?

Founded in 1881 by a husband and wife duo, PVH (NYSE:PVH) is a global fashion conglomerate with iconic brands like Calvin Klein and Tommy Hilfiger.

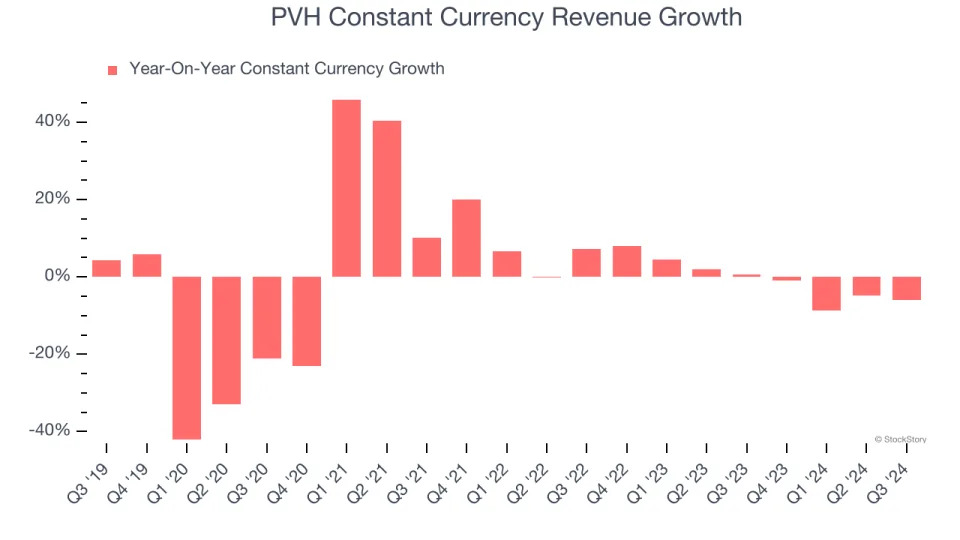

1. Constant Currency Revenue Hits a Standstill

We can better understand Apparel and Accessories companies by analyzing their constant currency revenue. This metric excludes currency movements, which are outside of PVH’s control and are not indicative of underlying demand.

Over the last two years, PVH failed to grow its constant currency revenue. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests PVH might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

2. Cash Flow Margin Set to Decline

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict PVH’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 8.2% for the last 12 months will decrease to 4.1%.

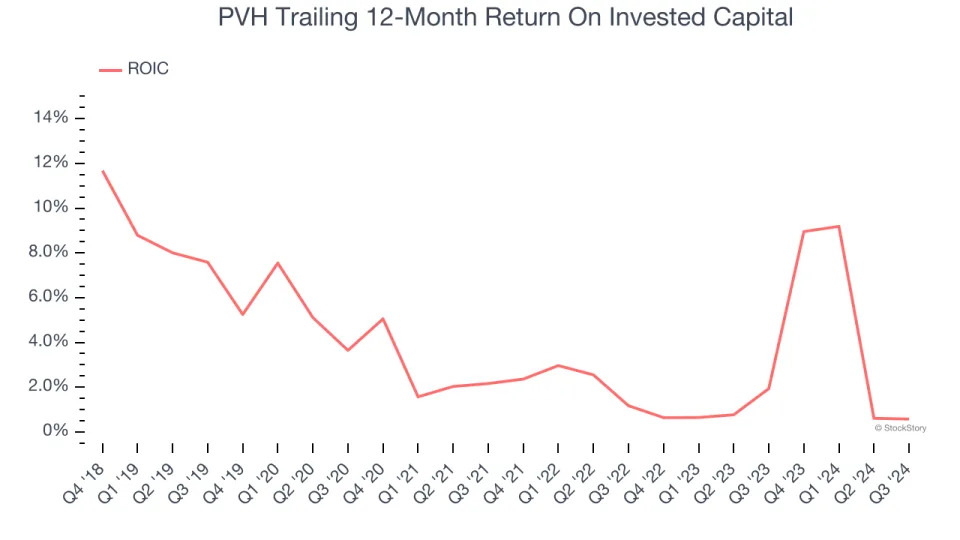

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

PVH historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 1.9%, lower than the typical cost of capital (how much it costs to raise money) for consumer discretionary companies.

Final Judgment

PVH doesn’t pass our quality test. With its shares trailing the market in recent months, the stock trades at 7.8× forward price-to-earnings (or $94.84 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. We’d recommend looking at the most entrenched endpoint security platform on the market .

Stocks We Like More Than PVH

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free .